When scholarships and financial aid fall short, understanding the cost of attendance and how to cover funding gaps can help students and families plan with confidence.

Paying for college is one of the biggest financial decisions families face. While financial aid can help reduce costs, it often doesn’t cover everything. Tuition is only part of the equation. Housing, meals, books, transportation, and everyday expenses all factor into the total cost.

With early planning and a clear understanding of how college costs work, students and families can better evaluate their options and decide how private student loans may fit into their overall plan.

What Is Cost of Attendance?

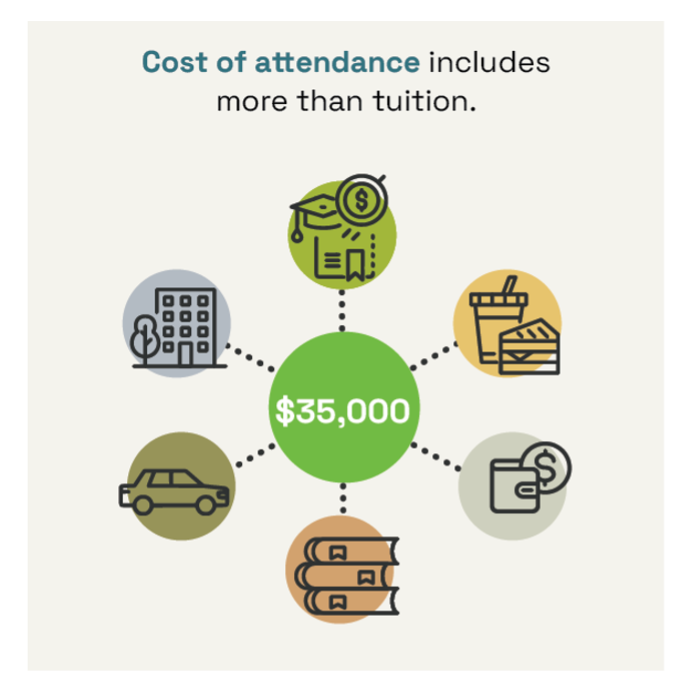

Cost of attendance is the total estimated cost to attend a school for one academic year. Schools use this figure to determine how much financial aid a student can receive.

Cost of attendance typically includes:

Tuition and required fees.

Housing and meal plans.

Books and supplies.

Transportation.

Personal and miscellaneous expenses.

This number serves as the foundation for every financial aid offer and is the starting point for understanding cost of attendance and how much you may need to pay out of pocket.

How Financial Aid Packages Work

Most students use a combination of resources to pay for college, including:

Scholarships and grants.

Federal financial aid, such as grants, work-study, and federal student loans.

Family 529 plans or savings.

Each school builds financial aid packages differently, which is why two offers can look very different even when the cost of attendance is similar.

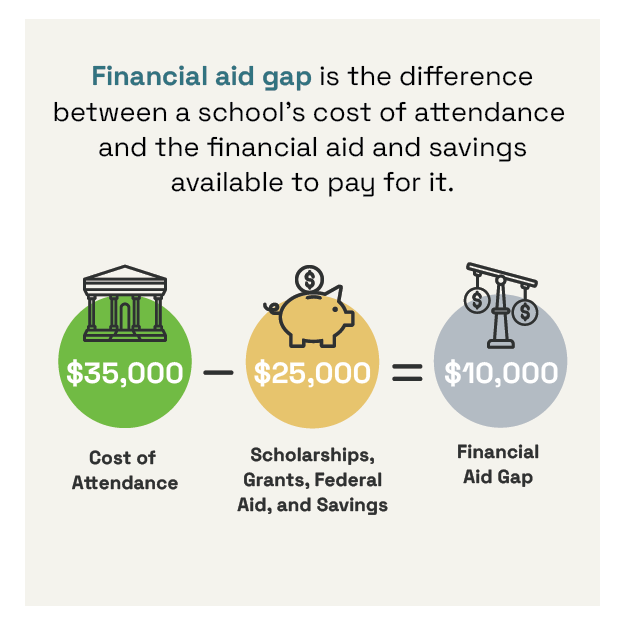

What Is a Financial Aid Gap?

A financial aid gap is the difference between a school’s cost of attendance and the total financial aid and savings available to help cover it.

To calculate your gap:

Start with the school’s cost of attendance.

Subtract scholarships, grants, federal aid, and savings.

The remaining amount is the financial aid gap.

Understanding this gap can help students and families plan for the portion of college costs they may still need to cover.

How to Compare Financial Aid Offers

Learning how to compare financial aid offers side by side can help students and families better understand the true cost of each school.

When reviewing offers, look closely at:

Tuition and required fees.

Housing and meal plan costs.

Scholarships and grants, including renewal requirements.

Work-study eligibility.

Federal loan amounts.

Estimated out-of-pocket costs.

Focus on gift aid first — scholarships and grants you don’t have to repay — then evaluate borrowing options if a gap remains. If anything is unclear, a school’s financial aid office can help explain the details.

What Expenses Do Student Loans Cover?

Student loans can help cover approved education expenses that remain after other aid is applied.

Depending on the loan type, student loans may be used for:

Remaining tuition and fees.

On-campus or off-campus housing.

Meal plans.

Books and supplies.

Other school-certified education costs.

Private student loans are often used to help fill the gap when scholarships, grants, federal aid, and savings don’t cover the full cost of attendance. Understanding what expenses student loans cover can help students and families decide whether borrowing makes sense for their situation.

How Much Should You Borrow for College?

There is no single right amount to borrow. A common approach is to borrow only what you need to cover your financial aid gap after:

Scholarships and grants.

Federal financial aid.

Savings or family contributions.

If a gap remains, understanding potential monthly payments and long-term repayment expectations can help students and families make informed borrowing decisions.

How Private Student Loans Fit Into the Picture

Private student loans are typically considered after free aid and federal options have been applied.

Federal student loans may offer fixed interest rates, income-driven repayment options, and borrower protections — such as deferment, forbearance, and forgiveness programs — that private loans typically don't. Private student loans can help students and families cover remaining costs when federal financial aid is not enough.

Learning how private student loans work can help borrowers decide whether they fit into an overall college funding plan.

When comparing private student loans, it can help to review:

Interest rates and repayment options.

Available loan terms.

Whether a cosigner may be needed.

Cosigner release options.

At Nelnet Bank, many undergraduate borrowers apply with a cosigner, which is common nationwide. Making on-time payments can help students build credit, and some lenders (like Nelnet Bank) allow borrowers to apply for cosigner release after meeting certain requirements.

Why Checking Your Rate Early Can Help

Checking your rate early can provide clarity before making decisions. It can help students and families:

Estimate potential monthly payments.

Compare borrowing options.

Plan ahead with confidence.

Nelnet Bank uses a soft credit pull to check rates, which does not affect your credit score.

Practical Ways to Manage College Costs

In addition to financial aid and loans, small steps can students and families help manage college costs:

Apply for scholarships throughout the year, including those with later deadlines.

Consider part-time work or work-study to cover weekly expenses.

Create a simple budget to track monthly and weekly spending.

These strategies can help reduce out-of-pocket costs while students are in school.